Roth Conversion 5 Year Rule Irs

Roth Ira 5 Year Rule Straight From The Irs Youtube

Roth Conversion Q A Fidelity

The 5 Year Rules For Roth Ira Withdrawals Nerdwallet

The 5 Year Rules For Roth Irasc J Wealth Advisors

The Tax Trick That Could Get An Extra 56 000 Into Your Roth Ira

Traditional Roth Iras Withdrawal Rules Penalties H R Block

After the five year period beginning with the first taxable year for which a contribution was made to a roth ira set up for your benefit.

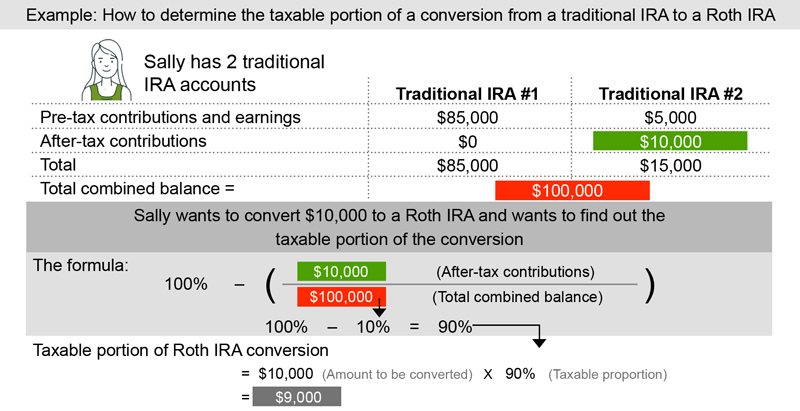

Roth conversion 5 year rule irs. Similar to the rule above withdrawals of money from the conversion of a traditional ira or 401 k to a roth ira are subject to a five year waiting period to avoid a penalty. The conversion is reported on form 8606 nondeductible iras. See publication 590 a contributions to individual retirement arrangements iras for more information. A conversion to a roth ira results in taxation of any untaxed amounts in the traditional ira.

When you are at least 59 1 2 years old. The 5 year rule on conversions is used to determine whether you ll pay the 10 percent penalty when you withdrawal the amount you converted. The 5 year rule applies in all cases where there is no individual designated beneficiary by september 30 of the year following the year of the owner s death or where any beneficiary isn t an individual for example the owner named his or her estate as the beneficiary. The second five year period applies to roth ira conversions and pretax employer plan rollovers to roth iras and defines when they may be withdrawn without being subject to the early distribution penalty tax.

If you take distributions from your roth ira earnings before meeting the five year rule and before age 59 be prepared to pay income taxes and a 10 penalty on your earnings. One five year period applies to the taxation of roth ira earnings and determines when the earnings can be distributed tax and penalty free. This special recapture rule does not apply when you roll over the distribution to another designated roth account or to your roth ira but does apply to a subsequent distribution from the rolled over account or ira within the 5 taxable year period. The roth conversion 5 year rule is about accessing penalty free conversion principal and is irrelevant if the individual already meets one of the other exceptions to the early withdrawal penalty while the roth contribution 5 year rule is about accessing tax free roth earnings which are assumed to be extracted last anyway.

The 5 year rule for roth ira distributions stipulates that 5 years must have passed since the tax year of your first roth ira contribution before you can withdraw the earnings in the account.

Financial Ducks In A Row Independent Financial Advice Ira

When Is The Tax Deadline For A Roth Conversion Your Money Your

Mega Backdoor Roth Convert Within Plan Or Out To Roth Ira

Splitting An Ira With 72 T Distributions In Divorce Divorce

Roth Conversions Things To Know Fidelity Investments Roth Ira

Third Avenue Funds Individual Retirement Account Ira Traditional

After Tax 401 K Contributions Retirement Benefits Fidelity

Minimize Taxes On A Roth Ira Conversion Betterment

Rolling After Tax 401 K To Roth Ira Fidelity

New Irs Rules On After Tax 401 K Rollover To Roth Ira Bankrate Com

Understanding The 401k To Ira Rollover Process Td Ameritrade

Tax Smart Ways To Convert A Traditional Ira To A Roth Ira

Tax Reform Killed A Key Roth Ira Legal Loophole Here S What To

Can Passive Losses Offset A Roth Conversion